Asian Stocks Dip as US Economic Resilience Challenges Rate Cut Expectations

Asian stock markets saw a slight downturn early Monday as investors adjusted their expectations regarding potential Federal Reserve interest rate cuts. This shift followed emerging signs of resilience in the U.S. economy, prompting traders to rethink strategies in an already fluctuating financial landscape.

Market Movements

Countries like Japan and Australia experienced declines in their stock indices. On the other hand, South Korea’s stock market defied the trend, buoyed by a surge in Samsung Electronics Co. shares after the company unveiled a stock buyback initiative. Interestingly, U.S. futures showed some recovery after the S&P 500 index fell 1.3% on Friday, effectively reversing more than half of its gains since the recent election.

The soft start to the trading week appears to extend last week’s global sell-off. Investors are increasingly pricing in the implications of potential tariffs and tax cuts introduced by Donald Trump, which could reignite inflation concerns in an already robust U.S. economy. A report released on Friday revising October’s U.S. retail sales figures upward has also contributed to growing skepticism that the Fed might pause its easing cycle until 2025. Currently, the odds of a rate cut next month lie below 50%.

Insights from Experts

Economists like Shane Oliver of AMP Ltd. in Sydney suggest that while another Fed rate cut in December is still plausible, it remains a contentious issue. “A slower pace of easing is likely next year,” he noted, highlighting that Trump’s proposals regarding tariffs and tax cuts may pose upside risks to inflation over the next one to three years.

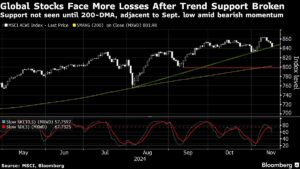

Additionally, the U.S. dollar experienced slight fluctuations after rising 1.4% in the previous week. This marked its seventh consecutive weekly gain, driven largely by a surge in Treasury yields resulting from diminished Fed policy expectations. The overall sentiment has had a cascading effect, impacting currencies across the board—from the Australian dollar to various emerging market bonds. Last week marked the worst performance for Asian stocks in nearly six months, with an overall decline of 3.9%.

Commodities Update

In the commodities arena, oil prices remain under pressure due to oversupply concerns and declining demand from China, the world’s largest crude importer. Furthermore, geopolitical dynamics continue to evolve, with Ukraine’s allies urging President Volodymyr Zelensky to explore new resolutions to the ongoing conflict with Russia. The U.S. is also deliberating whether to ease restrictions on some Western-made arms intended for limited military operations against Russia.

Key Events to Watch

This week is packed with significant financial events. Traders are particularly keen to hear from Bank of Japan Governor Kazuo Ueda, who is expected to disclose insights into the central bank’s upcoming policy decisions—especially in light of increasing worries about the rapid depreciation of the yen. Barclays strategists emphasize that Ueda’s press conference could provide crucial signals concerning the timing of the Bank of Japan’s next rate hike.

Other noteworthy events include:

- China’s Banks: Expected to maintain their loan prime rates after a prior cut in October.

- Bank Indonesia: Set to announce a critical policy decision, particularly as the Indonesian rupiah approaches a significant threshold against the dollar.

- Inflation Reports: The UK and Eurozone will release inflation data, essential for assessing future policies from the Bank of England and the European Central Bank.

Upcoming Market Indicators

The following is a list of key events slated for this week that could impact market dynamics:

- BOJ Governor Kazuo Ueda speaks – Monday

- Group of 20 Summit – Begins Monday

- European Union Foreign Ministers’ Meeting – Monday

- Australian RBA Meeting Minutes – Tuesday

- Eurozone CPI Data – Tuesday

- Canada CPI Data – Tuesday

- China’s Loan Prime Rates – Wednesday

- Indonesia Rate Decision – Wednesday

- UK CPI Releases – Wednesday

- Nvidia Earnings Report – Wednesday

- Various US economic indicators including consumer sentiment and manufacturing PMIs – Friday

Summary of Market Trends

Stocks:

- S&P 500 futures: Up 0.1%

- Hang Seng futures: Up 0.2%

- Japan’s Topix: Down 0.7%

- Australia’s S&P/ASX 200: Down 0.3%

- Euro Stoxx 50 futures: Down 0.7%

Currencies:

- Bloomberg Dollar Spot Index: Little changed

- Euro: Stable around $1.0535

- Japanese Yen: Stable at 154.44 per dollar

- Offshore Yuan: Steady at 7.2392 per dollar

Commodities:

- WTI Crude: Down 0.4% to $66.77 per barrel

- Spot Gold: Up 0.4% to $2,572.64 per ounce

It’s crucial for investors to keep a close watch on these developments this week. As market conditions evolve, making informed decisions based on the latest insights and data will be essential for navigating these uncertain waters.