Understanding CBDC and Its Implications for Your Wealth

As the conversation around Central Bank Digital Currencies (CBDCs) intensifies, questions arise about their impact on personal wealth. One reader, KS, raised critical concerns about whether CBDCs would lead to the conversion of savings from bank accounts, brokerage accounts, and even physical assets like gold and silver. Here’s what you need to know, and why this might matter more than ever.

Will Your Traditional Savings Be Converted to CBDCs?

Yes, it is highly likely that your traditional bank savings and brokerage assets will transition to a digital format under the CBDC system. Currently, the funds in your bank account are already mostly electronic entries. This shift is part of a broader trend where physical bank branches are closing, paving the way for a future dominated by digital finance. It’s increasingly clear that banks are transitioning to a model where physical cash becomes obsolete. Picture this: banks no longer need to maintain physical branches because the act of depositing or transferring money can be done from your smartphone.

This transition could leave many individuals scrambling to understand how to navigate their financial futures without the conventional banking setup they have relied upon. At Extreme Investor Network, we encourage our community to stay informed and proactive in adapting to these changes.

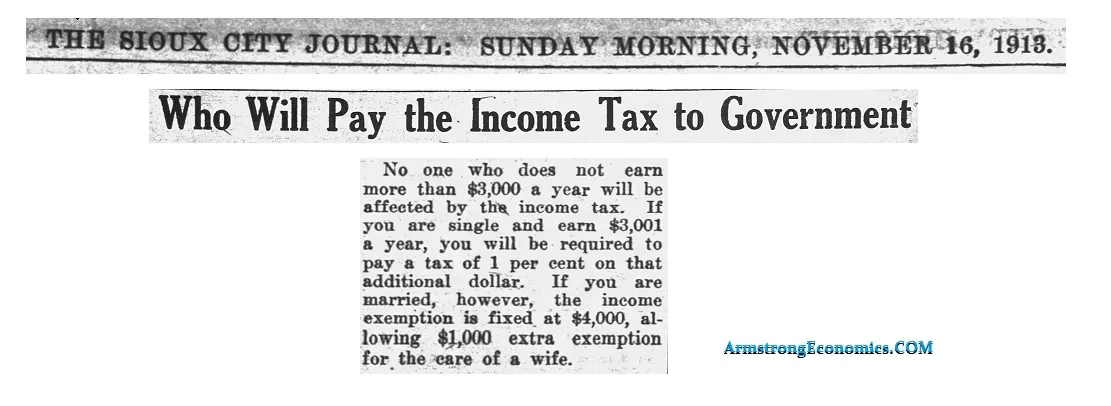

Understanding the Underlying Motives

Some analysts argue that the primary intention behind CBDCs is tax collection. By creating a fully digital economy, governments aim to eliminate cash transactions that escape taxation. Every financial interaction will be traceable, allowing authorities to monitor and tax even the smallest economic activities—potentially including hiring a neighbor’s teenager to babysit or finding cash on the street.

This initiative might be perceived as a step towards financial control, aiming to curtail the underground economy and enhance compliance. It’s essential to comprehend the implications of living in a digital economy that records every transaction—what does this mean for your financial privacy and autonomy?

The Legacy of Direct Taxation

Going back to the roots of the tax system in the U.S., direct taxation’s introduction has long been criticized for infringing on personal liberties. The founding fathers designed the government with caution against direct income taxes, yet these have become a staple of modern America.

When introduced, promises were made that only the wealthy would be taxed, yet this quickly transformed into widespread minor taxation affecting all layers of society. Today, we’re on the cusp of facing a new form of taxation model: one where every single transaction is potentially taxable.

The Shift Towards Complete Surveillance

The drive towards CBDCs can portray a system of economic servitude whereby governments can monitor virtually every aspect of citizens’ financial lives. This has historical precedence; think of how various taxes from the 19th and 20th centuries were justified under emergencies like wars. Over time, those taxes became permanent fixtures.

As noted during the implementation of the Gold Confiscation Act in 1933, the government didn’t go door-to-door; they handled it through institutions. Today, CBDCs may allow governments to challenge individual ownership of assets in ways we might not anticipate.

The Future of Real Property Ownership and Financial Assets

With the introduction of CBDCs, we might soon find ourselves in a scenario where the only safe haven from complete financial oversight would be in the form of tangible assets. Current numismatic coins, particularly those minted before 1933, could serve as a potential refuge from government tracking and taxation on digital or financial assets.

Will physical ownership become the new frontier in securing wealth? What are the practical steps you can take to safeguard your capital?

What To Do Next?

At Extreme Investor Network, we exist to keep our community informed and empowered. As the conversation about CBDCs continues to evolve, so must your understanding of asset protection and financial strategy. Here are some tips:

-

Diversify Your Holdings: Keep a mix of liquid assets, such as digital currencies, alongside tangible assets like gold or collectible coins.

-

Stay Informed: Follow reliable sources on financial legislation and changes in banking policies to anticipate your next steps actively.

- Engage in Discussions: Join forums and webinars that discuss CBDCs and their implications for individual wealth, taxation, and personal freedom.

The transition towards CBDCs is not merely a technological change; it symbolizes a fundamental transformation of our financial landscape. It’s time to evaluate how these changes might affect your financial future. Are you ready for what lies ahead?