“Bloomberg – Yen Falls as Japanese Ruling Coalition Fails to Secure Majority in Parliament”

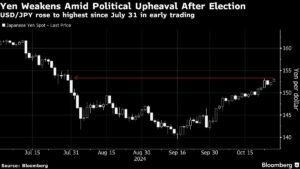

Political uncertainty in Japan has caused the yen to weaken after the ruling coalition failed to win a majority in parliament. This development has sparked speculation on how it may impact the central bank’s rate-hike policy. The Japanese currency dropped to 153.88 per dollar, reaching its lowest level in about three months. Prime Minister Shigeru Ishiba’s decision to call a snap election backfired, leading to the currency’s decline.

Despite this setback, the weakened yen has benefited Japan’s export-oriented economy, leading to a rise in the Topix index by up to 1.6%. The ultra-low interest rates in Japan compared to other major economies like the US are contributing to the yen’s weakness. The Bank of Japan is widely expected to maintain its policy interest rate at the upcoming meeting, signaling that the interest rate gap between Japan and other nations may persist for the foreseeable future.

Shuji Hosoi, a senior strategist at Daiwa Securities, noted, “This is an unexpected reaction. While political risk may be increasing, there may be expectations that the Ishiba administration won’t become a lame duck immediately.”

In other parts of Asia, Chinese shares experienced a dip in early trade after industrial profits plummeted in September, posing a challenge to the economy amidst deflationary pressures impacting corporate finances.

The drop in crude prices followed Israeli strikes on Iran, which avoided targeting oil facilities. Both Brent crude and West Texas Intermediate faced over a 5% reduction in early trading before recovering slightly. Gold also experienced a minor decline.

Looking ahead, investors are bracing for a data-heavy week with key economic indicators from various regions. Insights from Chinese economic activity readings, Eurozone and US growth reports, and a pivotal payrolls report will shape portfolio decisions heading into the year-end. Expectations surrounding the US election are also influencing trading strategies, particularly amid concerns about a potential return of Donald Trump to the White House.

Barclays Plc strategists highlighted, “As the elections approach and Trump trades increasingly are implemented, the US dollar may remain on the front foot while US rates remain elevated, creating a somewhat painful backdrop for emerging market assets.” The strategists noted that currency markets have already priced in some election premiums in recent weeks.

This week, markets will closely watch earnings reports from major companies and developments such as the Bank of Japan’s policy decision, Australia’s inflation data, and PMI readings from China. Notable events include Japan’s unemployment figures, US job openings data, Eurozone and UK economic indicators, and Amazon, Apple, and Samsung earnings reports.

In terms of market movements, stock futures are up across major indices, with the S&P 500 and Nikkei 225 futures posting gains. Currencies saw the Bloomberg Dollar Spot Index rising, the euro holding steady, and the yen weakening against the dollar. In cryptocurrency markets, Bitcoin remained stable, while Ether experienced a slight increase. Bonds and commodities, such as crude oil and gold, faced fluctuations throughout the trading sessions.

Stay informed with the latest financial news and market updates by visiting Extreme Investor Network. Subscribe to our newsletter to receive exclusive insights and analysis to help you make informed investment decisions.