Market Insights: U.S. Recession Concerns and Global Developments Influence Stock Movements

European stocks are gearing up for a potentially robust start, buoyed by President Donald Trump’s recent reassurances regarding the resilience of the U.S. economy. Additionally, Ukraine’s acceptance of a 30-day truce proposal with Russia has created optimism, setting the stage for a higher open in equity-index futures across Europe.

Optimism in Global Markets

As investors digest the latest geopolitical news, European equity-index futures climbed by as much as 1.2%, while contracts for U.S. stocks also experienced gains. Trump’s remarks indicating that he does not foresee a U.S. recession have helped to calm Wall Street jitters. Asian markets saw a rebound after a four-day decline, with Australia’s benchmark S&P/ASX 200 index hovering near correction territory due to the ongoing impacts of Trump’s steel and aluminum tariffs, for which no exemptions were granted.

In the face of these tariffs, the European Union has retaliated, raising its own levies on American goods. This escalating trade conflict illustrates the growing complexities of international relations and trade dynamics, which investors must watch closely.

Interest Rates and Market Volatility

The bond market reflected slight movements, with Treasury yields inching up, and the U.S. dollar strengthened against all Group-of-10 peers. The market remains on high alert due to Trump’s tariffs, the ongoing geopolitical situation in Ukraine, persistent inflation, and the unpredictable pace of Federal Reserve interest rate adjustments. The volatility index (VIX), a measure of stock market volatility, is hovering near its highest level since August, reflecting the anxiety surrounding U.S. economic growth.

According to Ken Wong, an Asian equity portfolio specialist at Eastspring Investments, any reduction in geopolitical tension is beneficial for the markets at this juncture. Developments such as the ceasefire in Ukraine and easing tariffs with Canada signal possible stabilization.

Economic and Corporate Policies

During a gathering of top executives at the Business Roundtable, Trump emphasized the need for expedited approvals, especially regarding environmental regulations. He hinted at announcing a significant electricity project soon and reiterated his position that businesses may face lower tax burdens if they manufacture domestically.

However, concerns persist as Goldman Sachs strategists have reduced their target for U.S. equity benchmarks due to increasing worries about economic growth, particularly regarding the so-called "Magnificent 7" stocks.

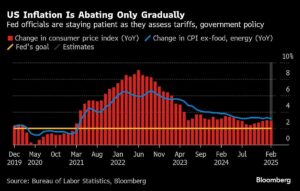

Inflation and Consumer Sentiment

On the economic calendar, investors are looking ahead to crucial U.S. consumer inflation data expected later this week. The consumer price index is anticipated to reflect a 0.3% increase in February, following a 0.5% rise in January. Market analysts, such as Kyle Rodda at Capital.com, have warned that signs of persistent inflation could restrict the Federal Reserve’s ability to cut rates, especially if Trump’s economic policies precipitate a slowdown in growth.

Commodities Landscape

In commodities, oil prices are on the rise following a revision of the U.S. forecast for global oversupply, while gold remains a safe haven as investors react to the market’s uncertain environment.

Key Events and Market Movements

Investors should keep a close eye on the following key events this week:

- Canada Rate Decision – Wednesday

- U.S. Consumer Price Index – Wednesday

- Eurozone Industrial Production – Thursday

- U.S. Producer Price Index and Initial Jobless Claims – Thursday

- U.S. University of Michigan Consumer Sentiment – Friday

Market Performance Snapshot

As of the latest updates:

- U.S. Stocks:

- S&P 500 futures rose by 0.1%

- Nasdaq 100 futures gained 0.1%

- Asian Markets:

- The MSCI Asia Pacific Index was largely unchanged

- Hong Kong’s Hang Seng fell by 1.1% for the fourth consecutive day

- The Shanghai Composite dropped by 0.2%

- European Stocks:

- Euro Stoxx 50 futures increased by 1.1%, marking a significant gain.

Currency and Cryptocurrency Moves

-

Forex Changes:

- The Bloomberg Dollar Spot Index increased by 0.2%

- The euro dipped by 0.2%, and the British pound fell to $1.2922.

- Cryptocurrencies:

- Bitcoin fell by 1.7% to $81,357.60, while Ether dropped by 4.3%, hitting a 16-month low.

Conclusion

The current landscape presents both challenges and opportunities for investors. With geopolitical tensions easing and significant economic indicators on the horizon, market reactions will largely depend on how these developments unfold. Keeping informed with timely insights and analysis, such as those available at Extreme Investor Network, can help investors navigate this complex terrain effectively.

Stay tuned to our platform for more comprehensive updates and market strategies tailored for the discerning investor.